IEEPA, Sections, and Drawbacks - What You Need to Know

Many importers are currently confused about which tariffs are being refunded, which are being newly applied, and what money you can get back from Customs and Border Protection (CBP) right now.

Let us answer your questions about this process, so you can more effectively get back the money you are owed.

Here is a quick summary, with further details below:

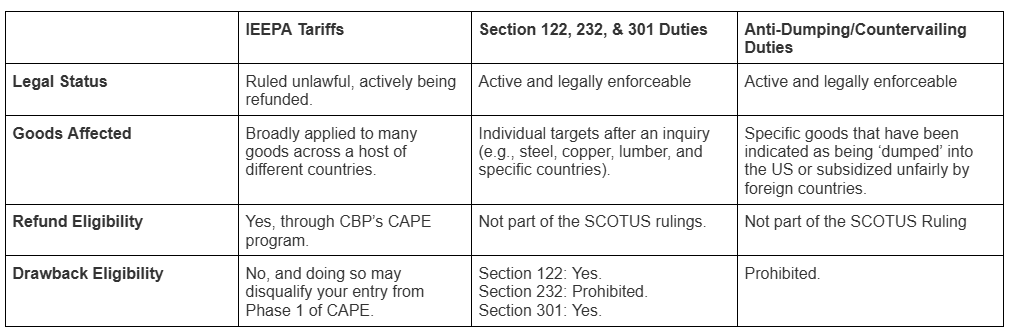

What is an ‘IEEPA Tariff’?

The International Emergency Economic Powers Act, or “IEEPA,” was the legal provision the US Government attempted to use to implement a set of international tariffs over the past year.

These tariffs were then struck down as illegal by the Supreme Court in 2026.

Are They Still in Effect?

No.

The tariffs that were imposed under IEEPA were struck down by the US Supreme Court on February 20, 2026, as illegal. Collection for these tariffs ended on February 24, 2026, following the Supreme Court order. As such, the US government is developing and deploying functionality to assist with the filing and refund process.

Can I get a Refund on an IEEPA Tariff?

To find out whether you are eligible for a refund or whether any of the duties you paid in the last year were IEEPA tariffs, we recommend a review. Once identified, these can be filed via the CAPE functionality in the ACE portal by the Importer of Record or the Broker of Record.

All of our services related to preparing for and receiving a CAPE refund can be found on our CAPE Refund Preparedness service page."

All of our services related to preparing for and receiving a CAPE refund can be found on our CAPE Refund Preparedness service page.

—

What is CAPE?

CBP’s Consolidated Administration and Processing of Entries (CAPE) program is the newly implemented process for importers owed refunds for the IEEPA tariffs. It allows for consolidated filing of your entries and the calculation of interest owed. It is the system in which the importer of the filing broker can request those refunds, and where the processing of those refunds will take place.

This is being rolled out in phases, with Phase 1, which began on April 20, 2026. Complete information on how this process is unfolding can be found on our blog post covering the complete details, and further updates are consistently being added as they happen on our Tariff Resource Page.

More information about CAPE and the services PCB can offer to help you with this is available on our CAPE Refund Page.

—

Anti-Dumping/Countervailing, Section 122, 232, 301 Duty?

The section duties (122, 232, and 301) are currently active duties that are applied to specific commodities and derivatives of specific countries, respectively.

At this time of this writing, a unilateral 10% tariff under the auspices of Section 122 is in effect on most goods from all countries.

Under Section 232, specific commodities are targeted for tariffs. For example, there are cases on steel, aluminum, copper, autos, lumber, etc. It is important to note that there are also new investigations currently underway looking at different industry sectors.

Certain Section 301 tariffs have been applied to specific countries. For example, the most well-known Section 301 case is levied against China.

These are not to be confused with Anti-Dumping/Countervailing duties, which are entirely separate from IEEPA and the section orders listed above.

Section 122

Section 122 is designed to address balance of payment issues and address trade deficits between the US and other countries. The catch, and primary difference between this and the IEEPA tariffs, is that it is capped at a maximum of 15% and can only be applied for 150 days before requiring a Congressionally approved extension. They were implemented on February 24, 2026, and therefore will be up for termination or extension on July 24, 2026.

Notably, the 15% cap is unique to Section 122; the other sections are not subject to such a limitation.

Section 232

These tariffs are implemented in the name of national security. The classic example of this is steel. If it can be proven through an inquiry that the importation of foreign-produced steel would damage domestic production irretrievably, then a Section 232 tariff could be introduced to keep US steel competitive.

Section 232 tariffs specifically exclude a duty drawback option.

Section 301

Section 301 tariffs are implemented to balance against unfair trade practices from other countries. The best example being China, which has had a 301 tariff implemented at varying degrees over the years.

There are currently investigations into over 60 economies for future Section 301 Tariffs.

Anti-Dumping/Countervailing Duties

Anti-dumping/Countervailing (AD/CVD) duties are highly targeted tariffs that are entirely separate from IEEPA and the section duties. AD is placed on highly specific goods that are sold in the US at an artificially low price in an effort to protect US industries. CVD is placed on goods that are priced artificially low as a result of a foreign subsidy.

It is easy to confuse these - especially Section 301, which sounds incredibly similar. The difference is the scope - AD/CVD are targeted to specific products, while the sections are levied against countries as a whole.

It is imperative that you understand that they are unaffected by each other. There is no refund or drawback option on AD/CVD. They seem similar, but they are utterly divorced in the eyes of CBP.

Due to the fact that these tariffs are currently legal and active, they are not currently eligible for refunds under normal circumstances.

Can I get a Drawback on the New Tariffs?

According to CBP, the newly implemented Section 232 and Antidumping / Countervailing tariffs specifically prohibit duty drawback, while Section 122 and 301 duties remain eligible for duty drawback.

However, as is always the case, drawback is strictly prohibited on goods affected by AD/CVD.

IMPORTANT NOTE: Do not apply for duty drawback on entries that could qualify for a CAPE refund. This may disqualify them from being included in Phase 1 of CAPE.

%20Logo%20Vector-DBG.svg)